Payday Super in Australia: What It Means for Your Super

Payday Super is a change to Australia’s superannuation rules that takes effect on 1 July 2026. From that date, your employer must pay your super at the same time as your wages, not once a quarter. For anyone in contract, labour hire, or casual work, where super has been harder to track, this is a meaningful shift. …

By Charisel Dela Pena

Career Development• Job Seeker • June 22, 2026

Payday Super is a change to Australia’s superannuation rules that takes effect on 1 July 2026. From that date, your employer must pay your super at the same time as your wages, not once a quarter. For anyone in contract, labour hire, or casual work, where super has been harder to track, this is a meaningful shift.

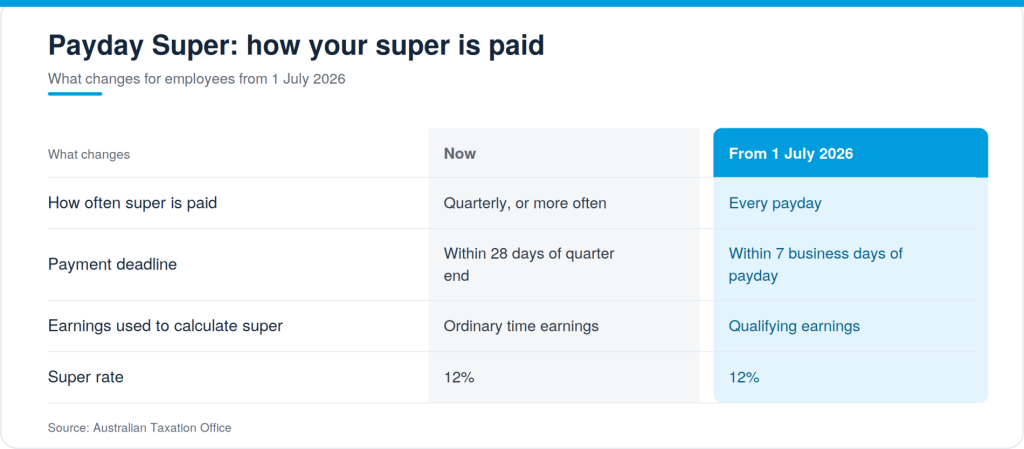

How is super paid now, and what changes from 1 July 2026?

Right now, employers can pay super quarterly, with contributions due up to 28 days after each quarter ends. From 1 July 2026, super must be paid on every payday, and under the ATO’s Payday Super rules your fund must receive each contribution within 7 business days of payday.

The super rate does not change; it stays at 12%. What changes is how often the money reaches your account and how it is calculated. One exception applies: for the first contribution for a new employee, or the first payment into a new fund, employers have a longer window of 20 business days, as set out in the ATO’s payment deadlines guidance.

What are qualifying earnings?

Qualifying earnings is a new term used to work out how much super you are owed. It brings together your ordinary time earnings with other payments such as commissions and salary sacrifice contributions. Super is still calculated at 12% of these earnings. For most people the difference is small, though it can mean a slightly larger contribution each pay.

Why is Payday Super good for your super balance?

Paying super more often gives your savings more time to grow. When contributions arrive every payday rather than quarterly, the money is invested sooner and compounds for longer, which over a working life can add up to a larger balance.

There is also more protection. The ATO tracks super payments through Single Touch Payroll, the same system used to report wages, giving it close to real-time visibility of whether super is paid correctly. The change aims to lift retirement outcomes and reduce unpaid super, as explained in the Treasury’s Payday Super policy. For casual or short-term roles, where late super has long been a problem, you are less likely to finish a job and find contributions missing.

How can you check your super is being paid correctly?

You can check your super yourself in a few minutes. Do this once Payday Super starts, especially if you change jobs or work for several employers.

- Log in to your myGov account, linked to the ATO, to see the contributions reported against your name.

- Check your super fund’s app or online portal to confirm payments are arriving and match your payslips.

- Watch the timing. From 1 July 2026, contributions should usually arrive within about a week of each payday.

- If something looks wrong, raise it with your employer first, then contact the ATO if it is not resolved.

The Fair Work Ombudsman’s summary of the new rules gives a plain-language overview of your entitlements.

Frequently asked questions

What is Payday Super?

Payday Super is a change to Australian super rules starting 1 July 2026. From that date, employers must pay super on the same day they pay wages, instead of quarterly. The rate stays at 12%, now calculated on qualifying earnings.

When does Payday Super start?

Payday Super starts on 1 July 2026, and applies to earnings paid from that date. For wages paid up to 30 June 2026, the existing quarterly super rules still apply.

How will Payday Super affect me?

You will see super paid every payday rather than every quarter. Your savings are invested sooner, which supports stronger growth through compounding, and you can more easily track whether your super is paid in full and on time.

Will I get super every pay cycle?

Yes. From 1 July 2026, eligible employees should receive super with every pay. Your fund must receive the contribution within 7 business days of payday. A longer 20 business day window applies to the first payment for a new job or into a new fund.

How can I check if my employer is paying super correctly?

Log in to myGov linked to the ATO and check your super fund’s app against your payslips. If super is missing or late, raise it with your employer, then the ATO.

Working with a recruiter who understands your entitlements

Payday Super is a reminder that pay and super matter when you take on a new role. Fuse Recruitment works with employers across insurance, manufacturing, and renewable energy who take their obligations to workers seriously. If you are looking for your next role and want a recruitment partner that keeps you informed, get in touch with our team.

This article is general information only and does not constitute financial advice. For your own circumstances, check the ATO or speak to a licensed financial adviser.

Related Content

When Was the Last Time You Checked Your Super?

For many Australians, super is something that was set up years ago, at a job they may not even hold anymore, and has not been looked at since. That is understandable. When you are settled in a role and life is busy, super feels like a problem for later. But later is exactly when small…

How to Move into a Renewable Energy Career in Australia

A career in renewable energy is within reach for many people already working in other industries. As one of the fastest-growing parts of the Australian workforce, the sector is drawing electricians, tradespeople, resources workers and engineers who want to move into cleaner, future-focused work. If that describes you, there is a good chance you already…

Why Client-Centric Finance Talent Is Harder to Hire

Financial services employers once hired for technical competence and trained the rest. That order has reversed. As advice, banking and wealth firms compete for a shrinking pool of qualified professionals, the people in highest demand are those who pair technical and regulatory knowledge with strong client skills. Hiring for that blend is now one of the sector’s hardest tasks. What is…

Related Content

When Was the Last Time You Checked Your Super?

For many Australians, super is something that was set up years ago, at a job they may not even hold anymore, and has not been looked at since. That is understandable. When you are settled in a role and life is busy, super feels like a problem for later. But later is exactly when small…

How to Move into a Renewable Energy Career in Australia

A career in renewable energy is within reach for many people already working in other industries. As one of the fastest-growing parts of the Australian workforce, the sector is drawing electricians, tradespeople, resources workers and engineers who want to move into cleaner, future-focused work. If that describes you, there is a good chance you already…

Why Client-Centric Finance Talent Is Harder to Hire

Financial services employers once hired for technical competence and trained the rest. That order has reversed. As advice, banking and wealth firms compete for a shrinking pool of qualified professionals, the people in highest demand are those who pair technical and regulatory knowledge with strong client skills. Hiring for that blend is now one of the sector’s hardest tasks. What is…

Where the Strongest Manufacturing Careers Are in 2026

Australian manufacturing is changing, and so are the careers within it. As factories adopt automation, robotics and connected systems, the sector is moving from traditional production lines towards advanced, highly regulated environments. For skilled workers, technicians and engineers, that shift is creating some of the strongest career opportunities in years, particularly across FMCG, life sciences and heavy…

How to Build Renewable Energy Teams in Regional Australia

Australia’s renewable energy build-out is concentrated where the projects are, and that is increasingly outside the capital cities. The Clean Energy Council estimates that up to 75 per cent of clean energy jobs could be based in regional Australia by 2035. For employers, the real challenge is building and holding a team in the location where the work…

Why Regulated Financial Services Roles Take Longer to Fill

In most industries, a vacancy is a resourcing problem. In financial services, it can be a regulatory one. Advice, risk and compliance roles carry licensing, qualification and accountability requirements that shrink the candidate pool and stretch hiring timelines well beyond other sectors. With major regulatory changes landing across 2025 and 2026, workforce planning has become inseparable from…