Payday Super Starts 1 July 2026: What Every Employer Needs to Know

Payday Super is now law. From 1 July 2026, employers must pay superannuation guarantee (SG) contributions on every payday, not quarterly, and each contribution must reach the employee’s super fund within 7 business days. The change is set by the Treasury Laws Amendment (Payday Superannuation) Act 2025, which has passed Parliament. Any payday on or after 1 July…

By Charisel Dela Pena

Employer • June 22, 2026

Payday Super is now law. From 1 July 2026, employers must pay superannuation guarantee (SG) contributions on every payday, not quarterly, and each contribution must reach the employee’s super fund within 7 business days. The change is set by the Treasury Laws Amendment (Payday Superannuation) Act 2025, which has passed Parliament. Any payday on or after 1 July 2026 is covered.

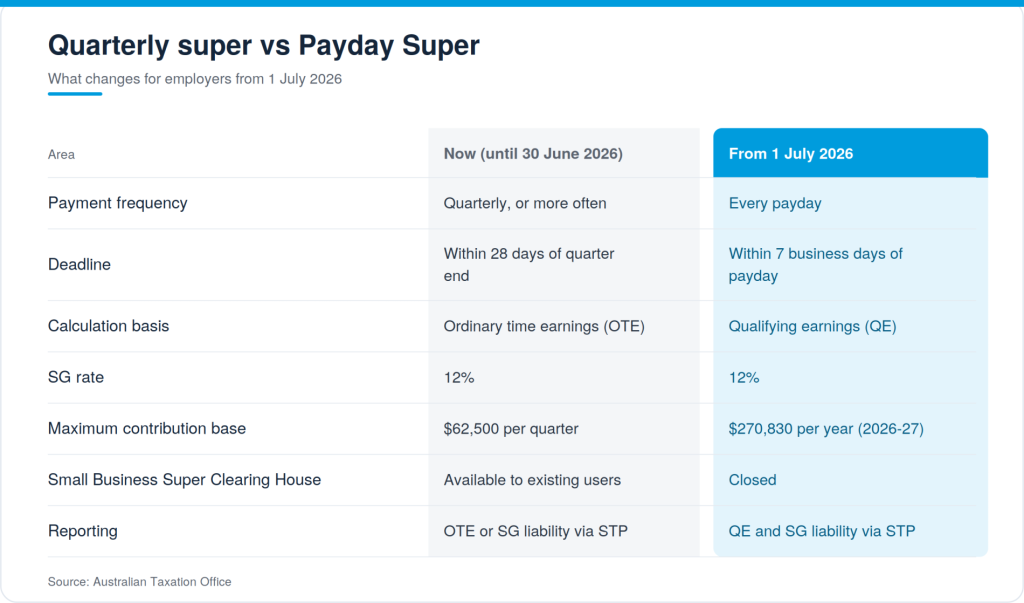

How does payday super differ from the quarterly system?

Currently, SG can be paid quarterly, due within 28 days of quarter end. From 1 July 2026, SG must be paid each payday and received by the fund within 7 business days. The main changes, from the ATO’s Payday Super guidance, are below.

The maximum contribution base, the cap on earnings that attract Super, moves to an annual $270,830 for 2026-27, per the ATO’s maximum contribution base guidance. With an annual cap, SG on high earners is front-loaded earlier in the year.

What is the seven-day rule, and what starts the clock?

The clock starts on payday, the day you pay qualifying earnings. The contribution must reach the employee’s fund, with the information needed to allocate it, within 7 business days. A business day excludes weekends and any state-wide or territory-wide public holiday. Because the deadline is the date of receipt, not the date you pay, allow processing time for your clearing house or payroll.

One extended deadline applies. For the first contribution for a new employee, or the first payment into a new fund, the window is 20 business days, as set out in the ATO’s payment deadlines guidance. From 1 July 2026, the New Payments Platform can be used, so payments can reach a fund the same day.

What are qualifying earnings, and how do they differ from OTE?

Qualifying earnings (QE) are the pay used to work out how much super an employee is owed. Until now that was ordinary time earnings (OTE), roughly the pay for normal hours. From 1 July 2026 it becomes QE, which is the same pay plus a few extras such as commissions and salary sacrifice amounts. The ATO lists what counts in its qualifying earnings guidance. The 12% rate is unchanged, so for most employers the super owed per employee rises a little.

What happens to the Small Business Superannuation Clearing House?

The Small Business Superannuation Clearing House (SBSCH) is closing. It stopped accepting new users on 1 October 2025, existing users can use it until 30 June 2026, and it is not accessible from 1 July 2026. Employers who rely on it must move to an alternative, such as a commercial clearing house or SuperStream-enabled payroll, before the start date. Leaving the switch late risks missed payments early on.

What are the penalties for getting payday super wrong?

If a contribution is late, the super guarantee charge (SGC) applies. Under the new rules the ATO assesses the SGC, calculates it on qualifying earnings, and adds interest that compounds daily plus an administrative uplift. On top of that, penalties of 25% or 50% of the unpaid charge can apply, depending on prior penalties. Because the ATO matches fund data against Single Touch Payroll, late super is visible quickly. The ATO has also published a first-year compliance approach to support the transition.

How should employers prepare before 1 July 2026?

- Confirm your payroll software can calculate SG on qualifying earnings and pay each cycle.

- If you use the SBSCH, choose and set up a replacement before 30 June 2026.

- Check employee super fund details are complete and correct to avoid rejected payments.

- Model the cash flow impact of paying super each pay run rather than quarterly.

- Confirm your fund or clearing house can receive payments via the New Payments Platform.

- Brief your finance and payroll teams, and update internal pay calendars.

Frequently asked questions

What is Payday Super?

Payday Super requires employers to pay superannuation guarantee at the same time as wages, instead of quarterly. From 1 July 2026, contributions must reach the employee’s fund within 7 business days of payday. The rate stays at 12%, calculated on qualifying earnings.

When does Payday Super start in Australia?

Payday Super starts on 1 July 2026. Any payday on or after that date is subject to the new rules. For wages paid up to 30 June 2026, the existing quarterly SG deadlines apply.

What are employer super obligations from July 2026?

From 1 July 2026, employers must calculate SG on qualifying earnings, pay it each payday, and ensure the fund receives it within 7 business days. The rate is still 12%, reporting is through Single Touch Payroll, and the SBSCH is no longer available.

What is the Payday Super seven-day rule?

The seven-day rule means an employee’s fund must receive each SG contribution within 7 business days of payday. A longer 20 business day window applies to the first contribution for a new employee or into a new fund. Business days exclude weekends and public holidays.

What are the penalties for non-compliance?

Late contributions trigger the super guarantee charge, assessed by the ATO on qualifying earnings with daily compounding interest and an administrative uplift. Penalties of 25% or 50% of the unpaid charge can also apply.

Working with a recruitment partner who plans ahead

As your team grows, so does the work of managing it, and reforms like Payday Super arrive quickly. Payday Super raises the cost of getting workforce admin wrong, which makes accurate planning more valuable as your team grows.

Fuse Recruitment helps employers across insurance, manufacturing, and renewable energy scale their teams and plan hiring as the rules change. If you are building your workforce or expect to hire soon, reach out to Fuse. We would be glad to help.

This article is general information only and does not constitute financial or tax advice. For your situation, check the ATO or a registered tax or financial adviser. The Fair Work Ombudsman also summarises the new rules and employer obligations.

Related Content

Payday Super in Australia: What It Means for Your Super

Payday Super is a change to Australia’s superannuation rules that takes effect on 1 July 2026. From that date, your employer must pay your super at the same time as your wages, not once a quarter. For anyone in contract, labour hire, or casual work, where super has been harder to track, this is a meaningful shift. …

Payday Super Starts 1 July 2026: What Every Employer Needs to Know

Payday Super is now law. From 1 July 2026, employers must pay superannuation guarantee (SG) contributions on every payday, not quarterly, and each contribution must reach the employee’s super fund within 7 business days. The change is set by the Treasury Laws Amendment (Payday Superannuation) Act 2025, which has passed Parliament. Any payday on or after 1 July…

How Digital Transformation Is Reshaping Insurance Job Design

Insurance has always been a data-driven industry. What has changed is the volume, velocity, and sophistication of that data, and the technology being built around it. Roles that existed in largely the same form for two decades are being redesigned. Some are being absorbed into automated systems. New ones are emerging with no direct precedent in the sector. For…

Related Content

Payday Super in Australia: What It Means for Your Super

Payday Super is a change to Australia’s superannuation rules that takes effect on 1 July 2026. From that date, your employer must pay your super at the same time as your wages, not once a quarter. For anyone in contract, labour hire, or casual work, where super has been harder to track, this is a meaningful shift. …

Payday Super Starts 1 July 2026: What Every Employer Needs to Know

Payday Super is now law. From 1 July 2026, employers must pay superannuation guarantee (SG) contributions on every payday, not quarterly, and each contribution must reach the employee’s super fund within 7 business days. The change is set by the Treasury Laws Amendment (Payday Superannuation) Act 2025, which has passed Parliament. Any payday on or after 1 July…

How Digital Transformation Is Reshaping Insurance Job Design

Insurance has always been a data-driven industry. What has changed is the volume, velocity, and sophistication of that data, and the technology being built around it. Roles that existed in largely the same form for two decades are being redesigned. Some are being absorbed into automated systems. New ones are emerging with no direct precedent in the sector. For…

How Insurance Careers in Australia Are Evolving Beyond Traditional Roles

The insurance industry is changing faster than its reputation suggests. For professionals already in the sector, the challenge is understanding where the real growth is and how to position for it. For those on the outside considering a move, insurance still carries an image that does not match the reality of where the work is heading. Is…

When Catastrophes Keep Coming: How Insurers Are Building Claims Teams That Last

The frequency and severity of weather events in Australia have changed. What were once described as one-in-fifty-year events are now occurring with regularity. The 2022 eastern Australia floods, successive storm seasons across Queensland and New South Wales, and repeated cyclone events in the north have each tested the claims handling capacity of the sector. Each…

Emerging Renewable Energy Jobs in Australia: Roles That Did Not Exist Five Years Ago

Five years ago, large-scale battery storage, offshore wind, and green hydrogen sat at the edges of Australia’s energy conversation. Today they sit at the centre of investment decisions, policy commitments, and workforce planning. The sector is not just growing. It is creating entirely new clean energy roles faster than the talent market can fill them. Jobs and…