EOFY Employer Checklist Australia 2026: What to Do Before and After 30 June

The end of the 2025-26 financial year brings a cluster of payroll and compliance obligations into a tight four-week window. Between late June and late July 2026, employers must finalise super, lodge Single Touch Payroll (STP) data, reconcile PAYG withholding, and lodge the June quarter activity statement. The same window marks the start of Payday Super on 1 July…

By Charisel Dela Pena

Employer • June 29, 2026

The end of the 2025-26 financial year brings a cluster of payroll and compliance obligations into a tight four-week window. Between late June and late July 2026, employers must finalise super, lodge Single Touch Payroll (STP) data, reconcile PAYG withholding, and lodge the June quarter activity statement. The same window marks the start of Payday Super on 1 July 2026.

Missing a deadline can trigger penalties, delay employees’ tax returns, and carry compliance exposure into the new financial year. This checklist sets out what to action before and after 30 June 2026, with the key dates first.

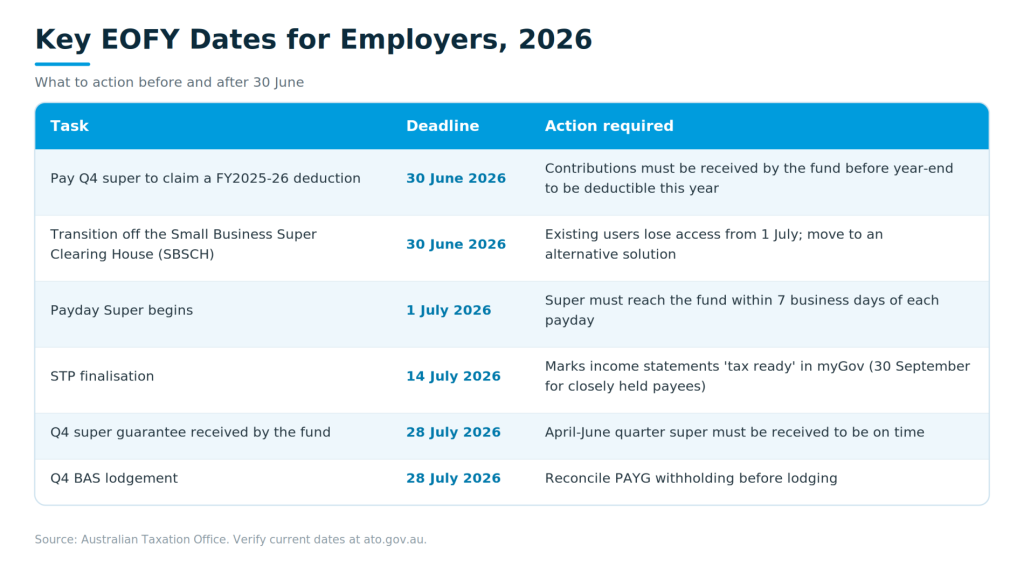

What are the key EOFY dates for employers in 2026?

These obligations fall in the June to July 2026 window. Most employers will need to action all of them.

What do employers need to do about super before and after 30 June 2026?

Two separate super deadlines apply this EOFY, and they serve different purposes. To claim a tax deduction in the 2025-26 financial year, your April-June super contributions must be received by the fund before 30 June 2026. To meet your super guarantee obligation and avoid the super guarantee charge, the same quarter must be received by the fund by 28 July 2026.

Clearing houses take time to process, so allow several business days before each cut-off rather than paying on the deadline. If you use the Small Business Super Clearing House, it closed to new users on 1 October 2025 and existing users have access only until 30 June 2026. You will need an alternative in place before the new financial year.

From 1 July 2026, Payday Super changes the rules entirely. Super guarantee contributions must reach each employee’s fund within 7 business days of payday, replacing the quarterly cycle. The rate remains 12 per cent. Your first July pay run triggers the new timeframe, so payroll systems, clearing house arrangements, and employee fund details should be confirmed before then.

How do employers finalise Single Touch Payroll for 2025-26?

STP finalisation tells the ATO that your payroll reporting is complete for the year. For most employees, the declaration is due by 14 July 2026. Once lodged, it marks each employee’s income statement as ‘tax ready’ in myGov so they can lodge their return. Closely held payees, such as directors and family members, have until 30 September 2026.

Before you finalise, reconcile your year-to-date figures. Check that gross wages, PAYG withholding, and super reported through STP match your accounting records, and correct any discrepancies first. Every employee paid during the year must be included, including casuals and staff terminated mid-year. Overlooking terminated employees is a common error that leaves their income statements unfinalised.

What are the PAYG withholding and BAS obligations at EOFY?

Your June quarter business activity statement is due on 28 July 2026. Before lodging, reconcile PAYG withholding for the year against your payroll records and STP reports so the figures align.

PAYG withholding also carries personal risk for company directors. Where withheld amounts or super are not paid to the ATO, directors can be made personally liable through a Director Penalty Notice. Reconciling and paying on time removes that exposure heading into FY2026-27.

Using your EOFY headcount review to plan FY2026-27 hiring

EOFY is when most workforce restructuring decisions are made. Headcount reviews, role changes, and new-year hiring plans are finalised alongside the compliance tasks above. It is the natural point to assess whether your team structure matches where the business is heading.

A few questions are worth working through now: which roles were stretched over the past year, where did contractor or casual reliance signal a permanent need, and what capability gaps will limit growth ahead? Mapping these against your FY2026-27 plan turns a compliance exercise into a workforce planning one.

As your team works through EOFY obligations, it is also the right time to assess whether your headcount is right for FY27. Fuse works with employers across insurance, infrastructure, renewables, manufacturing, and financial services to build capable, compliant teams.

Frequently asked questions

What do employers need to do before 30 June 2026?

Pay April-June super so it is received before year-end to claim a FY2025-26 deduction, transition off the SBSCH if you use it, and prepare payroll systems for Payday Super on 1 July. Reconciling payroll records ahead of STP finalisation also belongs here.

What is the STP finalisation deadline for 2026?

For most employees, STP finalisation is due by 14 July 2026. Closely held payees, such as directors and family members, have until 30 September 2026. Finalising marks income statements as ‘tax ready’ in myGov.

When is Q4 super due in 2026?

The April-June 2026 super guarantee must be received by employees’ funds by 28 July 2026 to be on time. To claim the deduction in FY2025-26, contributions must be received before 30 June 2026.

When does Payday Super start?

Payday Super begins on 1 July 2026. Super must then reach each employee’s fund within 7 business days of payday, replacing the quarterly cycle. The super guarantee rate stays at 12 per cent.

Ready to start your FY2026-27 workforce plan?

Once the compliance work is behind you, that same EOFY review becomes the clearest picture you will get of what your team needs next. You do not have to work through those questions alone.

Fuse works with employers across insurance, infrastructure, renewables, manufacturing, and financial services, and what sets us apart is that we understand the pressures behind the hiring, from budget cycles to compliance obligations to the lead times the hardest roles carry.

The strongest next step is a short conversation about the year ahead, so you head into FY2026-27 knowing what to hire, when to start, and what it will cost. Speak with Fuse today and start the new financial year with your workforce plan in motion.

This article is general information only and does not constitute financial or tax advice. For your situation, check the ATO or a registered tax or financial adviser. The Fair Work Ombudsman also summarises the new rules and employer obligations.

Related Content

Manufacturing Workforce Planning in Australia: Your FY2026-27 Hiring Plan

Australian manufacturing is not short of demand. It is short of people. A structural skills shortage, an ageing workforce, and accelerating automation mean the FY2027 hiring plan has to cover two things at once: the operational roles you need now, and the technology capability the business will need within 12 to 24 months. Setting that plan in July,…

Trades Workforce Planning in Australia: Your FY2026-27 Hiring Plan

For trades and services businesses, the skilled labour shortage makes early workforce planning a competitive advantage, not an administrative task. Australia’s trades shortage is structural, and reactive hiring is consistently slower and more expensive than planned hiring. Confirming your FY2027 workforce needs in July, rather than when a site is already under pressure, is what…

Renewable Energy Workforce Planning in Australia: Your FY2026-27 Hiring Plan

For the renewables energy industry, the start of the financial year is when project workforce plans need to be set. Budget approvals for new projects land in July, which is the window to scope workforce requirements and engage a specialist recruiter before mobilisation. Australia’s clean energy build is the largest workforce mobilisation the sector has faced, and the roles it depends on are already in short…

Related Content

Manufacturing Workforce Planning in Australia: Your FY2026-27 Hiring Plan

Australian manufacturing is not short of demand. It is short of people. A structural skills shortage, an ageing workforce, and accelerating automation mean the FY2027 hiring plan has to cover two things at once: the operational roles you need now, and the technology capability the business will need within 12 to 24 months. Setting that plan in July,…

Trades Workforce Planning in Australia: Your FY2026-27 Hiring Plan

For trades and services businesses, the skilled labour shortage makes early workforce planning a competitive advantage, not an administrative task. Australia’s trades shortage is structural, and reactive hiring is consistently slower and more expensive than planned hiring. Confirming your FY2027 workforce needs in July, rather than when a site is already under pressure, is what…

Renewable Energy Workforce Planning in Australia: Your FY2026-27 Hiring Plan

For the renewables energy industry, the start of the financial year is when project workforce plans need to be set. Budget approvals for new projects land in July, which is the window to scope workforce requirements and engage a specialist recruiter before mobilisation. Australia’s clean energy build is the largest workforce mobilisation the sector has faced, and the roles it depends on are already in short…

Financial Services Workforce Planning in Australia: Your FY2026-27 Hiring Plan

In financial services, the new financial year is the point at which hiring plans become real. FY2027 budgets are confirmed in July, turning headcount from aspiration into approved positions you can act on. It is also the moment to get ahead of the roles that take longest to fill. Regulatory reform, digital transformation, and an ageing workforce are reshaping these teams, and the…

Insurance Workforce Planning in Australia: Why FY2026-27 Starts Now

For insurance businesses, the new financial year is a planning window, not just a compliance one. Budgets reset on 30 June, and headcount approvals for FY2026-27 are confirmed in the first weeks of July. That makes now the most actionable point to set a hiring plan, confirm budgets, and line up specialist support before the market tightens. Reactive hiring…

EOFY Employer Checklist Australia 2026: What to Do Before and After 30 June

The end of the 2025-26 financial year brings a cluster of payroll and compliance obligations into a tight four-week window. Between late June and late July 2026, employers must finalise super, lodge Single Touch Payroll (STP) data, reconcile PAYG withholding, and lodge the June quarter activity statement. The same window marks the start of Payday Super on 1 July…